Balance Sheet and Profit & Loss Account for the First Quarter 2004

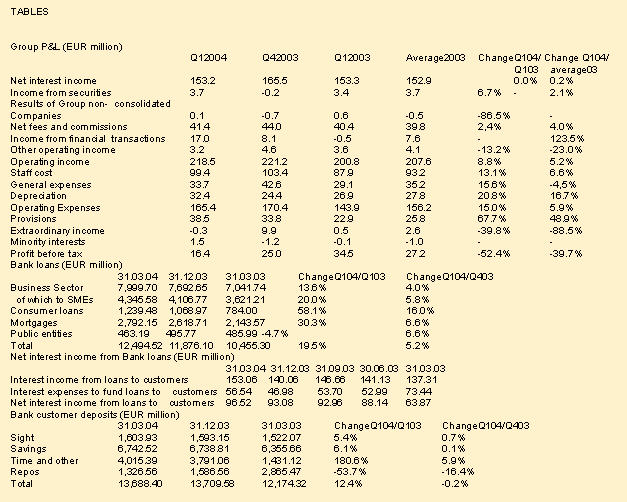

Operating income EUR 218.5 million (+8.8%)

Pre-tax profit EUR 16.4 million (-52,4%)

Framework for the Group Transformation

GROUP FIRST QUARTER 2004 RESULTS

Pre-tax profit, after minorities, decreased by 52.4% to EUR 16.4 million, as compared with EUR 34.5 million in Q1 2003, mainly due to the following:

1. Increased provisions to meet impairments in the value of investments of Emporiki Capital (EUR 6.3 million) and, in addition, to further strengthen loan loss reserves as a prudent step to facilitate the vigilant approach of the new management towards risk. As the restructuring of the Group unfolds, this proactive attitude would allow for additional flexibility in addressing potential credit quality issues.

2. Operating expenses up 15%, mainly due to:

increased staff cost, including contributions to fund deficits in Emporiki?s auxiliary pension fund

increased general expenses, including those related to the promotion of mortgages and consumer loans

first time consolidation of Credicom (for the period 01/09/2003 to 31/03/2004), which completed its incorporation.

Net interest income in Q1 2004 remained flat vs. Q1 2003 at EUR 153.2 million and net interest margin was virtually unchanged at 3.47%. Net interest income in Q1 2004:

Has benefited from

the strong growth of the total loan portfolio

the continuing shift in the loan mix in favour of consumer loans and mortgages.

Was adversely impacted by the decrease in revenues from fixed income securities resulting from the reduction of the bond portfolio.

Net fee and commission income rose by 2.4% year on year at EUR 41.4 million.

Income from financial transactions at EUR 17 million was up vs. Q1 2003, reflecting favourable conditions in the capital markets.

In Q1 2004, operating expenses rose by 15% vs. Q1 2003. Staff cost, including contributions to fund deficits in Emporiki?s auxiliary pension fund, are up 13.1%. Part of this increase includes a provision for an increase in nominal staff salaries in view of the forthcoming completion of the Collective Labor Agreement. General expenses, up 15.6% year on year, reflect the increase in expenses related to the promotion of mortgages and consumer loans.

Cost to income ratio deteriorated in Q1 2004 to 75.7% vs. 71.6% in Q1 2003.

Total loans expanded by 18.9%, on an annualized basis, to EUR 12.7 billion, strongly supported from the continuing shift of the loan portfolio mix towards lending to households and SMEs. This process is positively underpinned by the implementation of the ?PEGASUS? program. Up to 31 March 2004, ?PEGASUS? had been rolled out to 120 branches with encouraging indications on enhancements in their efficiency.

At the end of Q1 2004, customer deposits and repos of the Bank (representing 98% of the Group) rose by 12.3% to EUR 13.8 billion. During this quarter customers continued to rebalance their portfolios by shifting repos to deposits.

At end-March 2004, own funds stood at EUR 1.2 billion and the Tier I ratio is estimated at 8.6%. Approximately EUR 90 million was deducted from the Bank?s and Group?s own funds due to the purchase of own shares.

In view of the introduction of the International Financial Reporting Standards, an international audit firm has been mandated to provide a thorough analysis on pending issues that may have an impact on the financial accounts of the Bank and the Group. This analysis will serve as an additional input in the process of assessing the impact of these issues and in developing appropriate options to address them.

FRAMEWORK FOR THE 2004 GROUP TURNAROUND

The main objective of the new management is to strengthen the competitive position of Emporiki Bank enabling it to play a leading role in the region as a modern and dynamic financial services Group.

The new Group strategy is developed along the following dimensions:

- Achieve strong growth rates in the operating income in the core business: Retail Banking and Wholesale Banking

- Rigorously contain operating cost to achieve a favourable cost-benefit relationship in the various activities

- Optimize capital allocation within the Group, targeting in the medium term an RoE that exceeds 10-12%

- Clean up the balance sheet.

A number of specific initiatives are being launched in implementing the new strategy, including the:

- Introduction of a organizational structure

- Endorsement of a vigilant approach towards risks. In this context, the decision to proactively increase provisions in this quarter was identified as a step in this direction

- Strategic re-assessment of the role of subsidiaries. In this framework, the absorption of Emporiki Factoring by the Bank has been decided

- Acceleration of the process for the establishment of an EMTN program that allows also for the issuance of Tier II capital

- Set up of an MIS Division to develop comprehensive reporting tools to support management decisions

- Improvement of the bank network configuration

- Introduction of a new incentives scheme that allows for a clear-cut performance-related remuneration for sales-related personnel

- Introduction of a voluntary exit scheme offered to high rank executives

- Analysis by an international audit firm on pending issues that may have an impact on the Group?s financial accounts.

The new organizational structure aims specifically at:

- Introducing transparency and accountability and enabling the organization to implement the distinct dimensions of its strategy

- Enabling rigorous performance management of both business and support functions of the Group

- Aligning targets of the subsidiaries with those of the bank aiming to maximize performance at Group level

- Endorsement of a "Group culture."

Emporiki's management will continuously inform the financial community with progress updates.

George Provopoulos, Chairman and CEO of the Group, commented: "Our Group faces significant challenges that urgently require to:

- restructure and regroup our forces for efficiency and growth

- release resources currently tied up in low return activities with a focus to higher return opportunities.

Our valuable and competent human capital is fully capable of successfully implementing our extensive program for restructuring and dynamic development of the Group.

The initiatives that are in progress, and those to be launched soon, will provide the base for a better future for the Group, to the benefit of the shareholders, the customers and the employees.

I am confident that the positive results from our efforts will soon show up.

Download the

Balance Sheets

Download the

Balance Sheets