Financial results 2003

1. OVERVIEW

COSMOTE MOBILE TELECOMMUNICATIONS S.A., the leading provider of mobile tele-communication services in Greece, announces consolidated financial results for the twelve months ended December 31, 2003, reaffirming consistent and strong profitability.

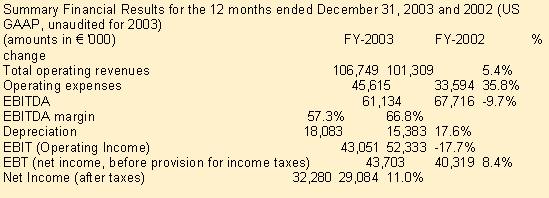

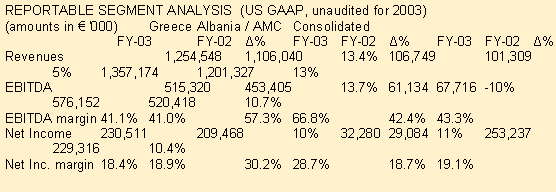

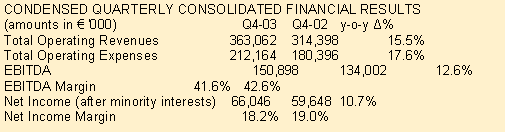

Group operating revenues for the period under review amounted to ? 1,357.2 mil, up 13% y-o-y, mainly driven by continually enhanced usage in Greek operations, combined with stable performance in the Albanian operations (please see table above). Fourth quarter operating revenues yearly growth (Q4-03) reached 15.5% exceeding the respective increase witnessed in the third quarter (10.7%), a strong indication of sustained growth trends.

Within a challenging competitive market and despite ongoing regulatory changes (that do not allow for a direct comparison y-o-y), COSMOTE's group EBITDA margin stood at 42.45%

Group Earnings amounted to ? 253.2 mil (+ 10.4% y-o-y), with net income margin at 18.7 %. It is also noted that group free cash flow was almost 11 times higher than FCF at the end of 2002 and reached ? 140.6 mil (post full 2002 dividend payment of ? 115.6 mil in cash). Net Debt stood at ? 211.2 mil significantly lower than 9m-03 and FY-02 (? 305.4 mil and ? 361.3 mil respectively).

2. FINANCIAL REVIEW

Total group operating revenues for the year ended December 31, 2003 increased by 13% to reach ? 1,357.2 million (including approximately ? 12 mil for the management of Globul and COSMOFON, see Appendix I). Excluding the change in OTE's accounting policy regarding Fixed to Mobile revenues (that are recorded net instead of gross since the end of Q1-03), y-o-y group operating revenue growth at the end of 2003 would have been approximately 16%.

The overall revenue increase mainly reflects the 13.8% increase in airtime revenues, the 21.2% increase in monthly service fees, the 7.4% increase in SMS revenues, the 36% increase in roaming revenues and the 5.5% increase in interconnection revenues. Revenues from telecommunications services increased by 12% during the period under review, representing approximately 97% of total revenues.

On a quarterly comparison (Q4-03 vs. Q4-02), total operating revenues grew by 15.5% y-o-y, higher than the respective yearly growth during the twelve month period ending 31 December 2003.

The key driver behind the healthy revenue growth is the significant increase in COSMOTE' s (domestic operations: GREECE) traffic volumes that during the twelve months ended December 31, 2003 increased by approximately 34% y-o-y.

The significant tariff cuts (on average -25%) effected with the introduction of the bundled packages were offset by the aforementioned traffic increase, evidence of ongoing positive usage elasticity. As a result COSMOTE's (domestic) revenues grew by 13.4% with airtime revenues increasing by 16.5%.

In addition data revenues (which include SMS, MMS, and other "soft data" revenues from Value Added Services) represent approximately 12% of total telecommunication revenues and 12.6% of domestic operations revenues.

The Company has (since launch) recorded over 270,000 MMS users that currently send on average around 25,000 MMS per day.

Roaming revenues grew y-o-y by 36%, accounting for 3.2% of total consolidated revenues, from 2.6% a year ago. During the fourth quarter of the year, the Company signed thirteen (13) additional roaming agreements that at the end of FY-03 amounted to 307, in 148 countries (6 more countries compared to 9m-03).

As previously mentioned consolidated profitability was sustained at high levels, with EBITDA reaching ? 576.2 mil, and EBITDA margin at 42.45%. The small decrease in the group EBITDA margin (0.9 p.p.) compared to one year ago is attributed to the dilution of AMC?s EBITDA margin by 9.5 p.p. (57.3% from 66.8% in FY-02, due to the introduction of mobile to mobile termination charges), that was almost fully offset by strict and efficient cost control.

Furthermore Greek operations EBITDA reached ? 515.3 million representing a 13.7% y-o-y growth. As a result domestic EBITDA margin reached 41.1% (excluding the effect of M2M: 48.2%), underlining the fact that domestic operational results remain strong and represent a solid foundation going forward.

Group Earnings amounted to ? 253.2 mil, up 10.4% y-o-y, despite the normalisation of the effective tax rate at 36.6% from 34.9% in 2002. Earnings per share also increased by 10.4% and therefore EPS during the period under review was ? 0.767 up from ? 0.695 a year ago. Consolidated Net Income margin in FY-03 stood at 18.7%.

Domestic operations earnings grew by 10%, to reach ? 230.5 mil, with net income margin at 18.4%. Greek operations earnings reaffirm the sustained strong operational and financial performance evidenced in the local market.

Finally, Free Cash Flow at the end of FY-03 reached ? 140.6 mil, almost 11 times higher than the 2002 FCF, reflecting the Company's enhanced cash flow generating capability and efficient working capital management (resulting in Cash at the end of 2003 of ? 156.7 mil).

Consequently Net Debt stood at ? 211 mil, -41.5% lower than last year. It is reminded that in Q3-03 the full dividend amount for year 2002 (approx. ? 115.6 mil, or ~50% pay-out ratio) was paid in cash.

Consolidated Capital Expenditures (including 2G, 2.5G, Olympic Games and 3G Capex) during the period under review have notably decreased to ? 184 mil , from ? 228 mil in FY-02, leading to a CAPEX/Sales ratio of 13.6 % compared to 19 % a year ago.

Consolidated 2G, 2.5G and Olympics capital expenditures amounted to approximately ? 169 million (Greece ? 156.9 million and Albania ? 12.2 million).

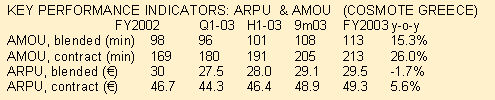

Blended AMOU during FY-03 has increased by 15.3% (y-o-y) to reach 113 min. This is driven by the continuous quarterly strong growth in contract AMOU that at the end of FY-03 was 44 minutes higher compared to a year ago (26% increase). It is noted that contract AMOU during the fourth quarter (Q4-03) exceeded 235 min, up from 231 min recorded in Q3-03. This strong positive trend, a continuation of the trend that started in 2002 and was enhanced on a quarterly basis throughout 2003, once again underpins the fact that voice usage represents the key growth driver in the Greek mobile market.

COSMOTE blended ARPU for the period under review (at ? 29.5) was slightly lower compared to a year ago, absorbing:

- the significant tariff cuts (-25% approximately)

- the dilution effect from the higher proportion of prepaid customers in the total customer base (~59.3% compared to ~55.8% at the end of FY-02) and

- the change in OTE's F2M accounting policy (? -0.75 effect on blended ARPU)

Blended ARPU was positively affected by the increase in contract ARPU that at end of FY-03 was ? 49.3 (+5.6% y-o-y). Contract ARPU during the fourth quarter (Q4-03) reached ? 50.5 as a result of the aforementioned continuing quarterly contract AMOU increase that to a large extent has offset the recent tariff rebalancing and the lower fixed to mobile interconnection charges.

ALBANIAN MOBILE COMMUNICATIONS Sh.a

COSMOTE has been consolidating its majority owned subsidiary in Albania since year 2000. During the twelve months ended December 31, 2003 AMC contributed approximately 7.9% to the Company's consolidated revenues and 10.6% to COSMOTE group EBITDA.